I keep hearing about the war everywhere and so I thought my first post should be a explainer on the current situation of the war

The below is my research from various finance sources and a lot many articles that I read over the past month. AI is used to summarize my notes and present them in a understandable manner. All of the information is publicly available. All of the opinions presented are of my own and in no way constitute financial advice and don’t represent any financial institution.

This is a current update on the war situation between Iran and Israel/U.S. There are a lot more intricacies to this subject but the following is to make readers aware of the current situation of the war. Given the pace and uncertainty of events, market reactions can shift quickly and often unpredictably.

The analysis presented here reflects current observations and interpretations of the situation and should be viewed as informational and opinion based, not as financial or trading advice. Markets in such environments are highly volatile and any positioning should be approached with appropriate risk management and caution.

Sunday News Update- Iran and US have failed to reach a deal at Islamabad. US Vice President says Iran failed to give commitment that it wouldn’t seek nuclear weapons. Whether the truce holds or the war resumes immediately is a decision that Americans have to make. Later on Sunday, Trump has said the US Navy will block the strait and begin destroying the mines that Iranians have dropped in the strait. Further he said action will be taken against every vessel that has paid a toll to Iran

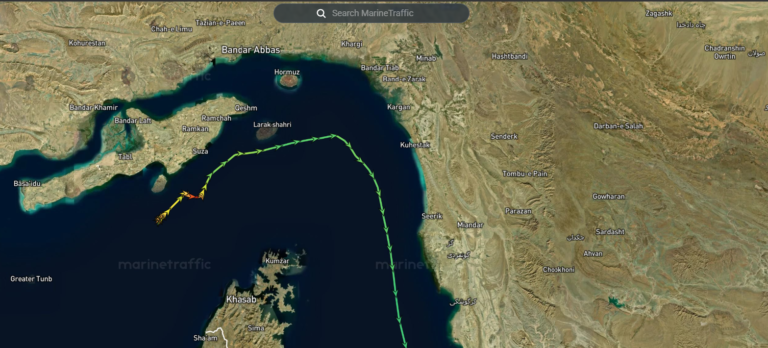

1. Strait of Hormuz Remains Operationally Constrained Despite Ceasefire

The Strait of Hormuz remains heavily constrained despite the April 7 ceasefire, with shipping activity still far below normal levels. Traffic has fallen from roughly 125 vessels per day before the conflict to just 4–14 ships daily in recent sessions, leaving hundreds of ships and containers stranded across the Gulf awaiting clearance. The lack of recovery reflects ongoing disagreement between Iran, the United States and Israel, as well as unresolved security risks in the region.

Iran’s Islamic Revolutionary Guard Corps has effectively signaled elevated danger across key transit routes, with shipping behavior consistent with the presence of sea mines or at least the credible threat of them. In response, U.S. Central Command has begun preparing mine-clearing operations, including the deployment of naval assets and underwater drones — a move that suggests the disruption is not just theoretical but operationally significant. Even alternative routes through Omani waters have been described as unsafe, further limiting flexibility for shipping operators.

There are early signs of limited movement returning, including a small number of tankers — notably Chinese and Greek vessels — transiting the strait over the weekend. In addition, U.S. naval ships have attempted to assert passage. However, this activity remains isolated and inconsistent. Reports indicate that at least two U.S. destroyers were warned and forced to turn back by Iranian forces, with UAV deployment reinforcing the level of active deterrence. This highlights that the strait is not functioning as a normal trade route but as a contested corridor, where access is uncertain and influenced by real-time military dynamics.

What makes this more significant is the timing. These developments are unfolding while U.S. and Iranian delegations are actively engaged in negotiations, suggesting a clear disconnect between diplomatic signaling and operational reality. For markets, this creates a critical misread: while headlines point toward de-escalation, the actual infrastructure of global oil flow remains impaired. Even if political tensions ease, the combination of reduced traffic, security risks and delayed shipments means that supply chains cannot normalize immediately.

2. Iran’s Shift From Disruption to Conditional and Monetized Access

Iran’s strategy in the Strait of Hormuz is shifting from disruption toward structured control, with transit increasingly becoming conditional rather than neutral. Iranian-owned vessels continue exporting crude — primarily to Chinese refiners — while ships from aligned nations such as China, India and Russia are being allowed passage, but only after extensive verification that they have no ties to U.S. or Israeli entities. Other international vessels face potential tolls of up to $2 million for large tankers, with more typical charges ranging between $120,000 and $250,000 per vessel, effectively adding around $1 per barrel to crude costs at current price levels.

At the same time, settlement mechanisms appear to be shifting away from traditional dollar channels, with reports of payments being accepted in Chinese yuan and alternative rails such as stablecoins, alongside discussions around formalizing Iranian oversight of the strait within domestic legal frameworks. This marks a significant break from long-standing international norms, where strategic waterways like Hormuz have historically remained open and toll-free. The proposal — including suggestions of external participation in toll collection frameworks — points toward an attempt to institutionalize control rather than use it as a temporary geopolitical lever.

The broader implication is that Iran may be testing whether Hormuz can function not just as a chokepoint, but as a recurring revenue-generating asset, drawing parallels to established models such as the Suez Canal (>$10 billion annual revenue at peak) and the Panama Canal (~$5.7 billion annually). For markets, the shift matters less for its immediate financial impact and more for what it represents: a move toward politicized and monetized trade routes, where access, pricing and settlement are increasingly shaped by geopolitical alignment rather than neutral global frameworks.

3. Internal Strategic Divide Within Iran Adds Policy Uncertainty

Iran’s strategy in the Strait of Hormuz is further complicated by an internal divide within its leadership, creating uncertainty over the direction of policy. Hardline factions favor maintaining restrictions or even prolonged closure of the strait until Israel halts attacks on allied groups such as Hezbollah in Lebanon, effectively treating the chokepoint as a direct geopolitical bargaining tool. This approach prioritizes leverage over economic cost, using disruption itself as a means of negotiation.

In contrast, more pragmatic elements within Iran appear to favor reopening the strait under controlled conditions, recognizing the strategic and fiscal value of managing transit rather than blocking it outright. Under this framework, regulated access — potentially including tolls and conditional passage — becomes a recurring revenue opportunity rather than a temporary pressure tactic. This reflects a shift from short-term coercion toward longer-term economic positioning.

The lack of alignment between these two approaches is delaying a clear and consistent policy stance, leaving shipping operators and energy markets navigating an uncertain operating environment. For markets, this ambiguity matters as much as the disruption itself. It sustains elevated risk premiums, as participants are forced to price not just current conditions, but the unpredictability of how Iran may choose to exercise control over the strait going forward.

4. Physical Oil Market Signals Acute Shortage Through Extreme Imbalance

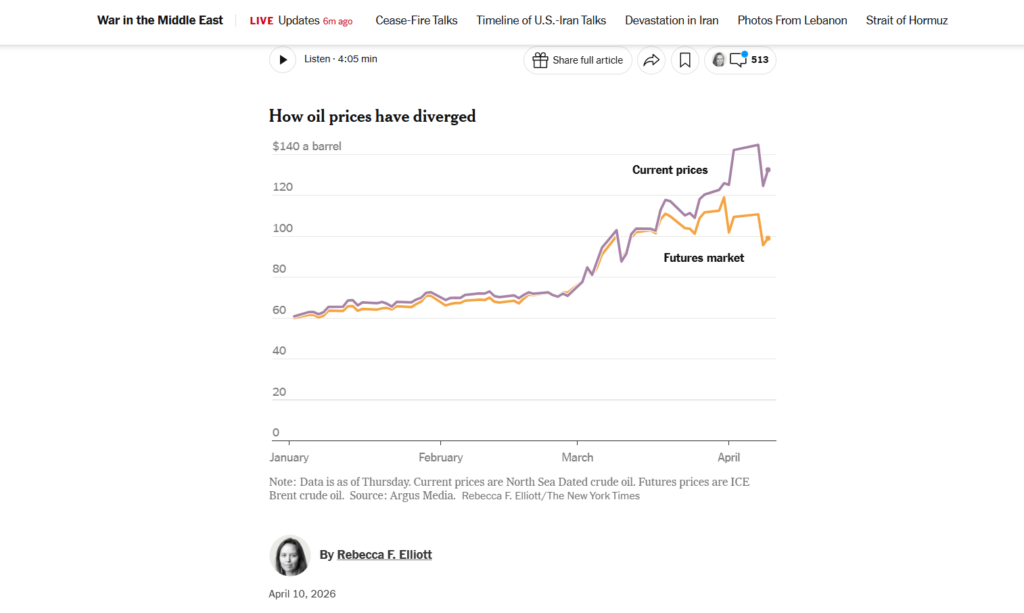

The clearest stress point is now visible in physical crude markets, where supply scarcity has moved beyond tightness into outright imbalance. In the North Sea — one of the most important global pricing hubs — traders submitted bids for roughly 40 cargoes within the week, but only around 4 found sellers, highlighting a severe shortage of available barrels. As a result, prompt cargoes are transacting near $140 per barrel, with premiums exceeding $20 above dated Brent, a level that reflects urgency rather than traditional price discovery.

Major trading houses such as Trafigura and Gunvor have been bidding aggressively for April and early May delivery cargoes, effectively competing on availability rather than valuation. This marks a shift in market behavior: pricing is no longer anchored to expectations of future supply-demand balance, but to the immediate need to secure barrels that can arrive on time. In this environment, the marginal buyer is not optimizing cost — they are minimizing the risk of running short.

The key takeaway is that this is not a structurally bullish signal on oil prices, but a timing-driven dislocation. The market is pricing the scarcity of barrels today, not the equilibrium of supply tomorrow, indicating that the physical system is under stress even as futures markets suggest a more normalized outlook.

5. The 40-Day Supply Gap Is Driving Current Market Behavior

At the center of the current dislocation is a timing mismatch between how markets price oil and how the physical system actually delivers it. The final tankers that left before the escalation are now arriving at their destinations, effectively marking the end of the last uninterrupted supply cycle. What follows is a gap: due to restricted transit through the Strait of Hormuz, the next meaningful wave of supply is not expected to reach end markets for roughly 40 days, creating a temporary but critical shortfall in available barrels.

This gap is forcing refiners to act defensively. With inventories at risk of tightening, buyers are securing crude at elevated premiums simply to maintain throughput, regardless of cost efficiency. In contrast, the futures market has moved in the opposite direction, with Brent declining toward $95 per barrel, down around 13% following ceasefire-driven optimism, reflecting expectations that supply conditions will eventually normalize. The result is a widening divergence between spot and forward pricing.

The key implication is that markets are pricing two different realities. Financial markets are forward-looking and reacting to political developments, while the physical oil system is constrained by logistics that operate with lag. Until new supply physically arrives, the shortage persists — meaning the current pricing disconnect is less about sentiment and more about time.

6. Extreme Backwardation Reflects Pricing of Immediacy Over Expectations

This timing-driven shortage is clearly visible in the structure of the oil market, which has moved into extreme backwardation. Dated Brent — the key benchmark for physical cargo surged to around $144 per barrel compared to brent futures at $109, briefly exceeding previous cycle highs, before easing to roughly $126 by the end of the week. Even after the pullback, it remains more than $20 above June Brent futures, which continue to trade closer to the mid-$90s range. This spread is not a technical anomaly — it reflects the premium attached to immediate availability in a system where supply cannot be replenished quickly.

In practical terms, the market is assigning a significantly higher value to oil that can be delivered today versus oil promised in the future. That only happens when there is a genuine shortfall in near-term supply. The backwardation is therefore not driven by speculative positioning or bullish sentiment, but by the physical constraint that barrels are simply not available in sufficient quantity right now, even if they are expected to return later.

The persistence of this wide spread suggests that markets have yet to fully internalize the lag between disruption and replenishment. While futures are reacting to expectations of normalization, the physical market continues to price the reality that supply chains are delayed, and until those delays clear, the premium on immediacy is likely to remain elevated.

7. Global Trade Flows Reconfigure Under Supply Stress

The disruption in the Strait of Hormuz is now forcing a rapid and visible reconfiguration of global oil trade flows, particularly across Asia, which remains structurally dependent on Gulf supply. The strait typically handles ~20–25% of global seaborne oil flows, with the majority of exports directed toward Asian economies such as China, India and Japan . With flows constrained, these countries are aggressively sourcing alternative barrels. Japan has increased crude purchases from the United States, while China has ramped up imports from non-Gulf producers such as Canada and Brazil, contributing to record export levels from these regions . India, meanwhile, has sharply increased imports from Venezuela, with shipments expected to exceed 12 million barrels this month, the highest in six years .

Logistics are adjusting alongside sourcing patterns. Japanese refiners, for example, are booking smaller vessels to move U.S. crude through the Panama Canal, prioritizing shorter transit times over traditional economies of scale. This reflects a broader shift in system behavior: supply chains are no longer optimizing for cost efficiency, but for reliability and speed. Even major trading houses and refiners are rerouting cargoes and repositioning vessels closer to alternative loading points, indicating that access to barrels has become more important than marginal pricing advantages.

The implication is that global oil trade is temporarily moving away from its optimized structure toward a stress-driven configuration, where flows are determined by accessibility rather than economics. This raises both costs and volatility across the system, as longer routes, smaller vessels and fragmented sourcing increase logistical complexity. More importantly, it reinforces that the current disruption is not just a regional issue — it is actively reshaping global energy flows in real time.

8. Refining Sector Faces Financial and Operational Stress

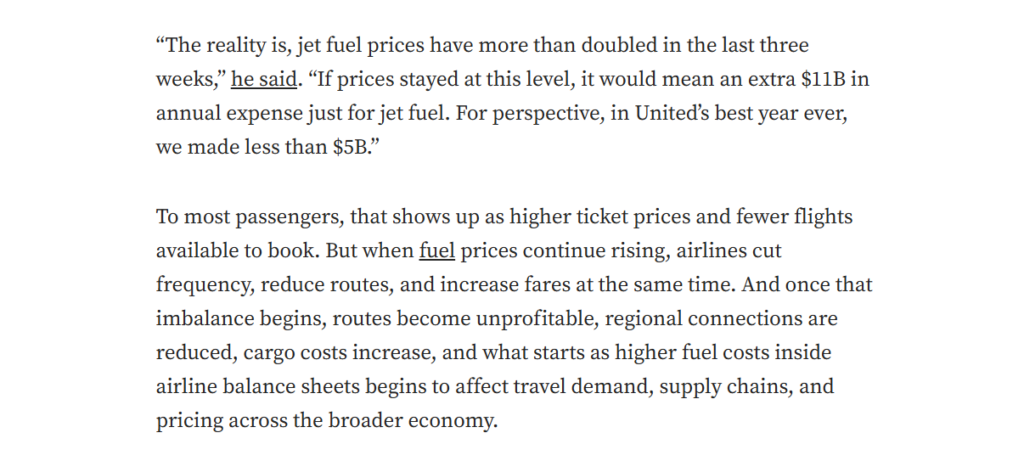

The pressure is now moving downstream into refining markets, where elevated crude costs are beginning to translate into tighter product supply and financial strain. Jet fuel and diesel prices have surged toward $180–$200 per barrel levels, reflecting not just higher input costs but also tightening availability of refined products. Summers are expected to make it worse along with driving gasoline prices further up. This marks a shift in the cycle: the shock is no longer confined to crude markets but is now feeding into fuels that directly impact transportation, aviation and industrial activity.

Smaller refiners are particularly exposed. At current crude prices, many are struggling to secure financing to purchase feedstock, as working capital requirements have risen sharply alongside price levels. This is already leading to early signs of reduced participation, with some operators stepping back from spot purchases. Importantly, this is not traditional demand destruction driven by falling consumption — it is financially constrained demand, where the willingness to buy exists but the ability to fund purchases does not.

If sustained, this dynamic will begin to impact output. Lower refinery throughput would reduce supply of key fuels such as diesel and jet fuel, tightening downstream markets further and amplifying price pressures. The result is a second-order effect: what begins as a crude supply disruption evolves into broader inflationary pressure across logistics, travel and industrial sectors, extending the impact well beyond energy markets themselves.

9. Government Policy Responses Reinforce Global Tightness

Policy responses are now beginning to amplify the underlying supply shock, with governments moving to protect domestic markets at the expense of global availability. India has sharply increased export duties on refined fuels, raising diesel duties from ₹21.5 to ₹55.5 per litre and jet fuel duties from ₹29.5 to ₹42 per litre, while leaving petrol unchanged. The immediate objective is clear: retain supply within the domestic system and capture higher fiscal revenues at a time of elevated prices.

However, the global implication is tightening. India is one of the largest refining hubs, and higher export duties effectively discourage overseas sales, reducing the volume of diesel and jet fuel available in international markets. At a time when physical supply is already constrained, this adds another layer of pressure, particularly for regions dependent on imports.

The broader risk is that this behavior spreads. In commodity shocks, governments tend to act defensively — prioritizing domestic stability over global efficiency. If multiple countries adopt similar measures, the result is a feedback loop: each action reduces global supply further, reinforcing higher prices and prompting additional restrictions. In that sense, policy is no longer just reacting to the crisis — it is actively contributing to the tightening of the system.

10. Supply Risks Extend Beyond Hormuz Infrastructure

Efforts to bypass the Strait of Hormuz are also coming under strain, underscoring how limited true alternatives are in the current environment. Saudi Arabia’s East–West pipeline — a ~1,200 km network built to move crude from eastern oil fields to Red Sea export terminals — was recently hit by a drone strike that damaged one of its eleven pumping stations, temporarily reducing throughput by an estimated ~700,000 barrels per day. The pipeline is one of the few large-scale routes capable of partially offsetting disruptions in Hormuz, making even localized damage materially relevant to global supply expectations.

Sunday Update– Saudi Arabia has fully restored the full pumping capacity back to its 7 million barrels a day. Output from Saudi Aramco’s offshore Manifa oil production facility was also restored after the attacks which reduced its production capacity by 300000 barrels a day each

While Saudi exports via the Red Sea continue, the incident highlights a deeper vulnerability: alternative infrastructure is not immune to the same geopolitical risks affecting primary routes. In practical terms, this reduces the reliability of contingency pathways and limits the system’s ability to absorb shocks. Even if Hormuz flows partially recover, the existence of simultaneous risk across backup routes increases the overall fragility of supply chains.

The implication for markets is that diversification alone does not eliminate risk — it redistributes it. When both primary and secondary routes face disruption potential, the system operates with less redundancy, reinforcing supply uncertainty and sustaining risk premiums across energy markets.

11. Geopolitical Risk Remains Active Despite Diplomatic Engagement

Despite ongoing diplomatic engagement, operational risk in the Strait of Hormuz remains elevated, with military dynamics continuing to shape access on the ground. Reports indicate that U.S. naval vessels attempting transit were met with warnings from Iran’s Islamic Revolutionary Guard Corps, including the deployment of UAVs, with at least some movements reportedly deterred or redirected. These incidents highlight that even state-backed vessels are not operating freely, reinforcing that the strait remains a contested environment rather than a normalized shipping lane.

What makes this more significant is the timing. These developments occurred while U.S. and Iranian delegations were actively engaged in negotiations in Islamabad, pointing to a clear disconnect between diplomatic signaling and real-world enforcement. In effect, negotiations are proceeding in parallel with active military posturing, rather than replacing it.

For markets, this distinction is critical. Diplomatic progress may reduce headline risk, but it does not immediately translate into operational stability. The continued presence of deterrence actions and contested transit conditions suggests that geopolitical risk is not being resolved — it is being managed within the system, keeping supply routes uncertain and risk premiums elevated.

12. Payment Systems Begin to Reflect Geopolitical Fragmentation

Iran’s reported willingness to accept payments in Chinese yuan and alternative channels — including stablecoins and limited crypto rails — adds a new layer of complexity to already strained energy flows. While these mechanisms remain marginal in scale, they reflect attempts to bypass traditional dollar-based settlement systems, particularly in an environment shaped by sanctions and restricted financial access. In practice, most large-scale commodity trades continue to rely on established banking networks, where compliance checks and traceability make widespread crypto usage difficult.

That said, the signal matters more than the scale. Even incremental movement toward non-dollar settlement frameworks suggests a shift away from historically neutral, standardized systems toward more geopolitically aligned payment structures. Transactions become conditional not just on price and supply, but on who is transacting and through which channels.

For markets, this represents an early stage of fragmentation rather than disruption. The dollar’s role remains dominant, but parallel rails — even if limited — introduce inefficiencies and increase transaction complexity. Over time, this could contribute to a more segmented global trading system, where energy flows, pricing and settlement are influenced as much by political alignment as by market forces.

13. Macro Transmission: Inflation Pressures and Policy Constraints Intensify

The energy shock is now feeding directly into broader macro conditions, with early signs of renewed inflation pressure emerging across major economies. In the United States, gasoline prices have risen by roughly 21%, reversing part of the earlier disinflation trend and pushing headline inflation expectations higher. This comes at a time when markets had begun to price a gradual easing cycle, creating renewed tension between growth concerns and inflation persistence.

Central banks are responding cautiously. Policymakers across multiple economies — including India, South Korea, Poland, Peru, Kenya, Serbia and New Zealand — have opted to hold interest rates, reflecting uncertainty around the durability of inflation declines. In the U.S., the Federal Reserve remains constrained: with inflation still near 4% and policy rates in the 3.5–3.75% range, there is limited room to ease without risking a re-acceleration in price pressures.

Institutional views are beginning to reflect this shift. Goldman Sachs expects the Fed to remain on hold until there is clearer evidence of both slowing growth and sustained disinflation, though it still sees scope for a rate cut later in the year if conditions stabilize. BlackRock, by contrast, maintains a more cautious stance, remaining underweight long-duration U.S. Treasuries and favoring European bonds, citing persistent inflation risks and the likelihood that long-term rates move higher.

Bond markets are already adjusting to this reality. The 2-year U.S. Treasury yield has moved toward ~3.8%, rising by roughly 50 basis points since the escalation, as expectations shift toward a “higher for longer” environment. The move in the front end of the curve — which closely tracks policy expectations — suggests that markets are repricing not just the timing of rate cuts, but the broader assumption that monetary policy can quickly normalize in the face of supply-driven inflation.

MY PLAYBOOK-

In case war continues/worsens (no negotiations/ strait remains closed) and supply of oil remains affected-

1) If the war continues or no war but the strait remains closed/ hefty fees charged, airline industry will feel the burn due to increased jet fuel prices. Jet prices have already moved sharply higher and EU airline industry warns of fuel shortages within 3 weeks if strait remains closed. The issue isn’t just price its availability. Particularly Europe imports around 50% of jet fuel from Persian Gulf, in case of rising costs and potential shortages we should see the airline industry suffering in equity markets. Good buying opportunity but will take a while to soar back to its previous levels as summer vacations are impacted from gasoline and jet fuel prices for the year.

2) Interest rates though expected to stay unchanged this quarter with a rate cut expected before the end of the year. However there might be hike in interest rates, if inflation consistently stays above 2% or increases above its current level, it may prompt central banks to raise interest rates over long term to slow price growth. Europe’s central bank is already expected to possibly do it currently as it primarily focuses on the price growth. Rates may remain elevated over medium term making current levels stable to lock in but not necessarily cheap.

3) Equities are booming on account of ceasefire news and positive outlook for the war. However physical system is still dealing with reality of disruption and lack of supply. Supply chains remain impacted, pipelines are damaged, production stalled, refineries temporarily closed. However, Saudi had a quick recovery in its east west pipeline and Aramco Manifa production which poses a question on is the recovery reliable and can we see a quick recovery in the other supply chains affected as well. Even if the strait is reopened it would still take time for the transmit to be it at its full capacity and thus there will be a gap in demand supply. There is a timing mismatch. Further if after 2 weeks ceasefire collapses the effects will be violent. Equities will bleed and oil goes higher. The only question is how fast? A good setup would be to follow the ceasefire negotiations closely and take a long position for May (preferred) or June futures. With its current price, upside is broader than downside.

Short term outlook-

Failure of US-Iran talks lift demand for save haven assets on Monday. Equity likely to take a hit and we may see gold get some breather due to benefit of geopolitical hedging over longer term as rate cuts of 50 bps are expected until the end of the year possibly in the last two quarters of the year. However rate cutes are still not confirmed as of now as the central banks may hold for longer and delay rate cuts if the war continues. It will be interesting to see how gold plays out. The key question is whether markets interpret this as temporary negotiation failure or collapse of ceasefire. Dollar is expected to rise after fall of 1.4% last week, along with rise in oil prices. We are also likely to see energy and defense sector stocks outperform the market possibly with a upward gap at the open. Energy is the most direct beneficiary of the supply concerns, but defense sectors seem to be interesting due to the rising geopolitical tension. Crude oil markets will closely watch the flows through strait of Hormuz.

FINAL TAKE-

If the war continues/ strait remains closed the consequences will be disastrous. Many critical industries such as food and transport will be affected directly affecting the cost of food and shipping/transport. Insurance and shipping costs ramp up which is not priced in properly yet. Shipping companies see higher profits, refineries dry up. Germany slowdown and Europe being highly energy imports heavy will be deeply affected. Volatility across major assets expected. Energy shocks ripple everywhere. Markets have not yet priced in delays in supply, policy constraints and system inefficiencies.

Time will tell what happens to STRAIT OF HORMUZ